Wells Fargo

Phillip C. Young

MBA F617

18 OCT 2108

Dr. Nicole Cundiff

HISTORY

Wells Fargo was founded in 1852 by Henry Wells and William Fargo. They founded during the gold rush in San Francisco to serve the West during the gold rush. The bank earned the trust of miners and others due to their responsible and expedient handling of money. Soon they had expanded to other new cities and mining towns. The bank spread rapidly after the opening of the transcontinental railroad. In the 1960’s Wells Fargo expanded out of the San Francisco area to become the regional bank of Northern California. By the 1980’s Wells Fargo spanned the entire state of California and was the nation’s 7thlargest bank. During the 1990’s Wells Fargo was continental with banks throughout the United States (Wells Fargo, 2018).

ORGANIZATIONAL VISION, VALUES AND GOALS

VISION

We want to satisfy our customers’ financial needs and help them succeed financially.

This unites us around a simple premise: Customers can be better served when they have a relationship with a trusted provider that knows them well, provides reliable guidance, and can serve their full range of financial needs.

VALUES

Five primary values guide every action we take:

- What’s right for customers. We place customers at the center of everything we do. We want to exceed customer expectations and build relationships that last a lifetime.

- People as a competitive advantage. We strive to attract, develop, motivate, and retain the best team members — and collaborate across businesses and functions to serve customers.

- We’re committed to the highest standards of integrity, transparency, and principled performance. We do the right thing, in the right way, and hold ourselves accountable.

- Diversity and inclusion. We value and promote diversity and inclusion in all aspects of business and at all levels. Success comes from inviting and incorporating diverse perspectives.

- We’re all called to be leaders. We want everyone to lead themselves, lead the team, and lead the business — in service to customers, communities, team members, and shareholders.

GOALS

We want to become the financial services leader in these areas:

- Customer service and advice. After listening to and understanding our customers and their financial goals, we want to provide exceptional service and guidance to help them succeed financially.

- Team member engagement. Our team members are our most valuable resource. We want to be the employer of choice — a place where people feel included, valued, and supported; everyone is respected; and we work as a team.

- Through innovative thinking, industry-leading technology, and a willingness to test and learn, we create lasting value for customers — and increased efficiency for our operations.

- Risk management. While working to set the global standard in managing all forms of risk, we want to serve customers’ needs and protect their assets, information, and privacy.

- Corporate citizenship. We make a positive contribution to communities through philanthropy, advancing diversity and inclusion, creating economic opportunity, and promoting environmental sustainability.

- Shareholder value. We want to deliver long-term value for shareholders through a balanced business model, strong risk discipline, efficient execution, and a world-class team (Wells Fargo, 2018).

MACRO VIEW OF WELLS FARGO

Wells Fargo is the third largest bank in the United States. According to the latest numbers from S&P Global Market Intelligence, a financial industry research firm has the third largest total assets of any bank in the US. (Dixon, 2018). Wells Fargo has 1.95 trillion dollars in assets, ranking closely behind its biggest competitors JP Morgan [2.53 trillion] and Bank of America [2.28 trillion] (Dixon, 2018). They have more than 13,000 ATM’s and approximately 5,800 retail banking branches coast to coast (Wells Fargo, 2018). According to Statista, Wells Fargo has over 232,000 employees, making it the largest employer for a bank in the United States. Wells Fargo is the 3rdlargest depository institution with the 4thmost total assets of any major bank in the United States. Internationally Wells Fargo has financial institutions in 38 countries (Wells Fargo, 2018).

REVIEW OF STRUCTURE

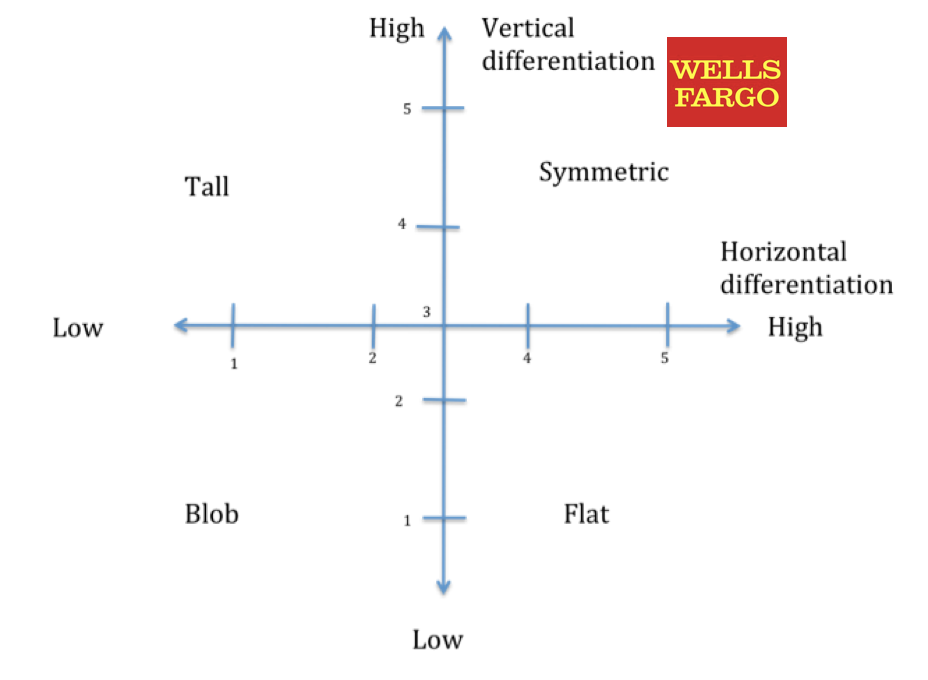

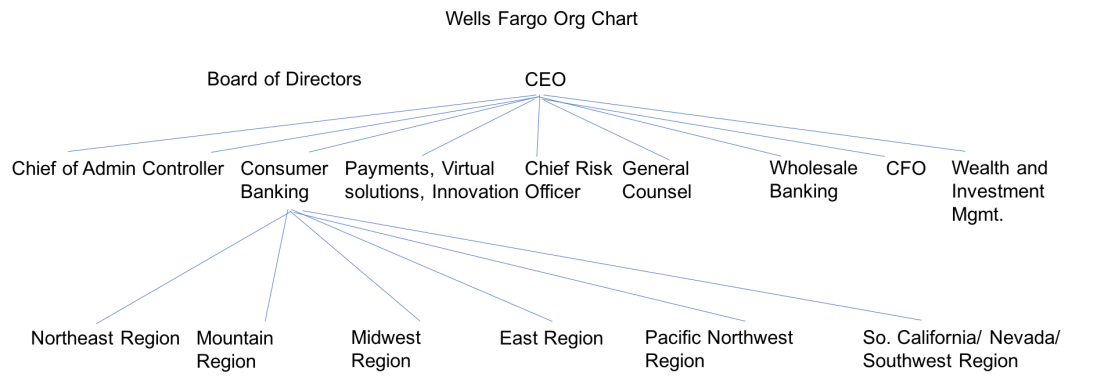

Wells Fargo is a symmetric matrix organization with both high vertical and horizontal differentiation. This is in part due to the size and complexity of the organization. Along with over 265,000 employees (Wells Fargo, 2018), the bank has multiple areas of specialized banking underneath its company. These include the following:

Banking, loans and credit, insurance, investing and retirement, wealth management, and rewards and benefits. Under the commercial segment, Wells Fargo offers loans, insurance for the owner as well as assets, credit facilities, merchant services, Online banking services, round the clock customer service etc. Under the small industries segment, their line of services includes banking, loans and credit, merchant services, insurance, and payroll and other services (Bhasin, 2018).

In order to oversee and manage this organization, Wells Fargo has an executive leadership team that consists of 10 executive officers that oversee all aspects of their business operations. These include the CEO, CFO, Administrative Officer, Wholesale Banking, Wealth and Investment management among other duties and responsibilities (Wells Fargo, 2018). The company also answers to a board of directors. There are 12 members on the board from different backgrounds.

Wells Fargo Business Banking division has the following 6 regions: East, Midwest, Mountain, Northeast, Pacific Northwest, Southern California and Southwest (Saxena, 2017). Each of these regions is headed up by a business banking leader that reports to the Executive VP of consumer banking (Wells Fargo, 2018).

REVIEW OF CULTURE (Post-Scandal)

Wells Fargo is committed to being the best they can be – for each other, their customers, their communities and their shareholders. Their mantra is ‘building better every day’ (Wells Fargo, 2018). In February of 2018 Wells Fargo entered into a consent agreement with the Federal Reserve to improve several aspects of their company, These included risk management, compliance and oversight. Since 2016 Wells Fargo has set aside 142 million dollars for customer remediation and settlement expenses. Wells Fargo has also began conducting reviews of their business practices in order to identify areas that still need to be addressed post scandal (Wells Fargo, 2018). The bank says that it is also committed to transparency and in the latest annual report chronicle many of the things they are doing in order to be a more honest organization. Their website also updates things for consumers to be aware of, such as updates on class action suits. The following goals were set in the annual report by CEO Tim Sloan:

- Our consistent vision of helping customers succeed financially.

- Our five values, which articulate what’s most important to us: what’s right for customers, people as a competitive advantage, ethics, diversity and inclusion, and leadership.

- Our six goals: becoming the financial services leader in customer service and advice, team member engagement, innovation, risk management, corporate citizenship, and shareholder value.

REVIEW OF ENVIRONMENT

Wells Fargo has a turbulent environment caused by multiple factors. One of the primary external threats to Wells Fargo are the security and Cyber threats. As previously annotated in the Wells Fargo SWOT: hackers stole $172 billion from people in 2017. As many as 978 million people in 20 countries lost money to cybercrime last year, according to a new report by security firm Norton. The individual impact: Norton says that victims lost an average of $142 to hackers in 2017, and that each victim spent almost 24 hours dealing with the fallout. How the US was hit: The report claims that 143 million Americans were affected by cybercrime in 2017, losing a total of $19.4 billion. (Conliffe, 2018).

In the context of turbulence as risk, the following five areas are noted as the top risks to banks in the ABA Banking Journal. The personnel named were quoted and the data was compiled by Julie Knudson, who is a contributor for the ABA. It is the author’s assumption that the following people were specifically quoted for this article and not cited from other sources. The first of these is security and cyber risk. The second is third party risk. The third issue is the concern over upcoming regulation. The fourth is that talent management [is] an ongoing challenge. The final risk cited from Julie Knudson is lending risk.

Cybersecurity continues to be a primary risk focus for financial institutions of all sizes. Dennis Hild, managing director in risk consulting, specializing in financial services at Crowe Horwath, LLP, says part of the concerns going into 2018 revolve around the risk-threat lifecycle and the current stage of cyber in that evolution. “It’s not very mature with regard to regulatory expectations and robust risk management,” he explains. (Knudson, 2018)

The banking industry has grappled for years with managing outside providers and the hazards those relationships may pose. “From a regulatory perspective, the key is that the regulators expect depository institutions to know who their third parties are,” says ABA VP Krista Shonk. But improving oversight of third-party risks—with banks striving to make their efforts not only more effective but also more efficient—is about more than keeping an inventory of vendors. “One thing we continually hear from regulators is that banks must have people on staff with adequate expertise to oversee their third parties,” Shonk says. (Knudson, 2018)

Regulatory uncertainty is top of mind. A number of issues are looming on the near-term regulatory horizon, many of which banks may not have had to confront in years past. While much has been written about CECL’s looming implementation and its impact on risk, the prospect of regulatory relief should also be on bankers’ radars. (Knudson, 2018)

In spite of all these factors it appears Wells Fargo has adapted to turbulence very well. They are still the top deposit gatherer in the United States and have a strong core business. (Compton, 2018) Wells Fargo is fundamentally sound. The company has excess cash, a conservative loan book and is aggressively returning capital to shareholders. The stock is a long-term buy. (Pinto, 2018)

ORGANIZATIONAL PROBLEM – CONTROVERSY

PROBLEM STATEMENT

Wells Fargo has experienced significant turmoil due to scandals that have come out against the company. These scandals have hurt both consumer confidence and stock price. There was also a cap placed on growth by the Federal Reserve; they cannot grow to any larger than 2 trillion assets, which was what their capacity was at the end of 2017 (Borak et. al., 2018). The biggest of these scandals was the creation of more than two million bank accounts and credit card applications done on the consumers’ behalf without their knowledge. This was the initial scandal that started a string of other investigations and penalties to the company. Regulators also charged Wells Fargo with putting bad consumer loan practices in regards to home loans. The bank misstated incomes and quality of originated home loans which can be attributed to the mortgage crisis of 2007-2008. The bank settled and agreed to pay a 2.09 billion dollar fine (Horowitz, 2018). Wells Fargo was also charged a one billion dollar fine for forcing customers into unneeded auto insurance and charging unnecessary mortgage fees (Egan, 2018).

CRITICAL EVALUATION

There are several negative orders of effects on Wells Fargo due to the scandals the company has faced. The first order is the fines levied towards the bank for the bad practices themselves. For the fraudulent account scandal, the bank was fined $185 million by the Los Angeles City Attorney and the Office of the Comptroller of Currency (OCC) (Blake, 2016). Wells Fargo settled out of court on the home loans scandal for 2.06 billion dollars (Horowitz, 2018). The market capacity limit that was placed by the Federal Reserve does not help the situation, as the company cannot grow and add accounts to offset these losses. Senator Elizabeth Warren wrote a letter to the Federal Reserve to push them to take the punishments farther and fire the entire boards of directors (Egan, 2017).

Arguably, Wells Fargo has been hurt more by the indirect costs of the scandals than the actual fines themselves. For first quarter 2018, the operating losses went up by 77% and overall expenses rose by 3%. Profits also declined by 12% during the quarter missing Wall Street’s expectations for them. Many analysts attribute these losses to the legal battles and scandals the company has faced. During this time deposits and lending have also dropped; two percent and one percent respectively. Their expenses rose for things such as advertising and promotion as the company tries to win back the trust of consumers. These costs rose 51% last quarter (Egan, 2018).

These stats look bad for Wells Fargo. The problems look even worse when factoring in the success of their main competitors during this period. JP Morgan posted a record 8.7 billion in profits for the first quarter of 2018. This was a record for any US bank. For the second quarter, they had a profit increase of 18% and almost matched their Q1 gains with 8.3 billion in profits (Egan, 2018).

RECOMMENDATIONS

In order for Wells Fargo to overcome the scandals and controversy, the company has to make a holistic change. Almost every facet of their business industry has been cited for misconduct. While the media campaigns and promises of transparency sound good, only time will tell if the bank actually learned their lesson from these events. The following are recommendations for repairing the company.

- Replace Top Level Management

CEO Tim Sloan has been with Wells Fargo serving as a senior manager since 2011. He has been the CFO, Head of Wholesale Banking, and the COO prior to his taking over as the CEO (Goldstein, 2018). It is arguable that he knew about the scandals during his tenue as a top executive. Senator Elizabeth Warren is pushing for his removal and made the following comments: “There are only two possibilities: either he was aware of this misconduct and he did nothing to stop it, or he was not aware of it despite his obligations as a senior manager of the company.” (Goldstein, 2018). It is a very plausible point that she is making. Either he was incompetent or unethical. This may not be the case, but removing senior staffers that have been part of the systemic corruption of multiple areas of banking could have a significant impact. Amazon recently came under pressure from political pundits for its low wages. After raising their minimum wage to $15 dollars an hour, Jeff Bezos was the beneficiary to lots of positive press (Bidwell, 2018). Any acting board members who were in place through the scandals should be replaced.

- Fix Risk Management Program and Oversight

In order to regain consumer confidence Wells Fargo will have to show action in regards to consumer protections. The company will also have to take aggressive action to improve internal controls, as well as, strengthen the risk management program (Borak, et. al., 2018). It’s not enough that Wells Fargo has went on an aggressive media campaign to win over customers. Consumers need to have physical controls in place to show that they do not have corruption risk when doing business with the company.

- Continue Aggressive Media Campaign

As mentioned above, Wells Fargo has spent a tremendous amount of money on advertising and promotion, doubling their expenses in this category. This is not exactly a standalone success metric as referenced by their declining revenues and rising operating costs. If it is combined with making actual compliance and regulation changes [above] it can be a very effective tool. The company has published sting press releases and have personnel on their payroll who can write well. Their effectiveness should go up tremendously after actually making significant changes.

IMPLEMENTATION

The first step is to STOP CORRUPT BUSINESS PRACTICES! The problem statement only contains a few of the bad practices that the bank has engaged in since the early 2000’s. Wells Fargo was also fined for illegally repossessing cars from 860 military service members. They faced a lawsuit from this year from small business owners who were duped by deceptive language in loan documents that charged them large termination fees (Borak, et. al., 2018). All the positive media and press in the world can’t make a difference if every demographic of people continue to file lawsuits and press charges for illegal business practices. Wells Fargo needs to distance itself as a company from all senior leadership that has been with them through the scandals that could have even remotely knew of their existence. Once this is complete a restructured risk and compliance plan should give consumers more confidence that the bank is going in the right direction. The media campaigns will have meat and be able to help the company rebound faster.

CONCLUSION

Wells Fargo is a very large successful bank that operates both locally in the United States and abroad through many other countries. While they have had some significant setbacks with legal issues and scandals, they have the ability to bounce back. Changes have to be made in not only the business practices, but the personnel in executive positions as well. The current operating environment has shown to be very beneficial to the banking industry with lower regulations and a much lower corporate tax rate. In the event that Wells Fargo can overcome their current issues, and stay out of the Federal Reserve and political crosshairs, they could be poised for a comeback sooner than later.

References

Bidwell, M. (2018, October 9). The New Amazon Minimum Wage: What’s the End Game? Retrieved from http://knowledge.wharton.upenn.edu/article/will-other-companies-follow-amazon-in-raising-the-minimum-wage/

Blake, P. (2016, November 03). Timeline of the Wells Fargo Accounts Scandal. Retrieved from https://abcnews.go.com/Business/timeline-wells-fargo-accounts-scandal/story?id=42231128

Borak, D., & Weiner-Bronner, D. (2018, February 3). Federal Reserve drops the hammer on Wells Fargo. Retrieved from https://money.cnn.com/2018/02/02/news/companies/wells-fargo-federal-reserve/index.html

Compton, E. (2018, October 12). Wells Fargo will spend 2018 in the penalty box, but it still has a strong core business. Retrieved from http://analysisreport.morningstar.com/stock/research/c-report

Condliffe, J. (2018, January 23). Hackers stole $172 billion from people in 2017. Retrieved from https://www.technologyreview.com/the-download/610043/hackers-stole-172-billion-from-people-in-2017/

Dixon, A. (2018, July 26). The 15 Largest Banks in America. Retrieved September 10, 2018, from https://www.bankrate.com/banking/americas-top-10-biggest-banks/#slide=1

Egan, M. (2018, July 13). Wells Fargo’s scandals are hurting its bottom line. Retrieved from https://money.cnn.com/2018/07/13/news/companies/wells-fargo-earnings-stock/index.html?iid=EL

Goldstein, S. (2018, October 18). Elizabeth Warren says Fed should keep Wells Fargo restrictions in place until CEO Sloan is ousted. Retrieved from https://www.marketwatch.com/story/warren-says-fed-should-keep-wells-fargo-restrictions-in-place-until-ceo-sloan-is-ousted-2018-10-18

History of Wells Fargo. (2018). Retrieved from https://www.wellsfargo.com/about/corporate/history/

Hitesh Bhasin. (2018, June 28). Retrieved September 17, 2018, from http://www.marketing91.com

Horowitz, J. (2018, August 1). Wells Fargo to pay $2.09 billion fine in mortgage settlement. Retrieved from https://money.cnn.com/2018/08/01/investing/wells-fargo-settlement-mortgage-loans/index.html

Knudson, J. (2017, December 11). Top Bank Risks in 2018. Retrieved from https://bankingjournal.aba.com/2017/12/top-bank-risks-in-2018/

Largest U.S. banks by number of employees 2017 | Statistic. (2018). Retrieved from https://www.statista.com/statistics/250220/ranking-of-united-states-banks-by-number-of-employees-in-2012/

Leadership and Governance. (2018). Retrieved from

https://www.wellsfargo.com/about/corporate/governance/

Saxena, A. (2017, June 05). Wells Fargo’s business banking group expands to four regions. Retrieved from https://www.reuters.com/article/us-wells-fargo-expansion/wells-fargos-business-banking-group-expands-to-four-regions-idUSKBN18W1Y0

Vision, Values & Goals. (2018). Retrieved from https://www.wellsfargojobs.com/values

Wells Fargo Today. (2018). 1-5. Retrieved from https://www08.wellsfargomedia.com/assets/pdf/about/corporate/wells-fargo-today.pdf.

Appendix A – Organizational Chart

Appendix B – SWOT Analysis

| Strengths

|

Weaknesses

|

|

Third largest bank in US

Strong credit rating

Amount of services provided for the consumer

|

Bank scandal fallout

Lack of Consumer Confidence

Stock Price Drop

|

| Opportunities | Threats |

|

New management

Lower Corporate Tax Rate

|

Online innovation

Traditional marketplace competitors

Online scams; identity thefts |